When a lender forecloses on Texas real estate, many borrowers assume the foreclosure sale ends the matter. Unfortunately, that is not always true. If the foreclosure sale does not generate enough money to satisfy the debt, the lender may seek a deficiency judgment against the borrower for the remaining balance.

What many property owners, guarantors, and even some investors do not realize is that Texas law provides a powerful statutory defense that can substantially reduce—or even eliminate—a deficiency claim.

That defense is found in Texas Property Code § 51.003.

What Is a Deficiency Judgment?

A deficiency judgment is the difference between:

- The amount owed on the loan at the time of foreclosure; and

- The amount credited from the foreclosure sale.

For example, suppose a borrower owes $500,000 and the property sells at foreclosure for $350,000. The lender may claim a deficiency of $150,000, plus potentially recoverable fees and costs.

However, Texas law does not automatically accept the foreclosure sale price as the property's true value.

The Protection Found in Texas Property Code § 51.003

Texas Property Code § 51.003(a) provides:

"If the price at which real property is sold at a foreclosure sale under Section 51.002 is less than the unpaid balance of the indebtedness secured by the real property, resulting in a deficiency, the person against whom recovery of the deficiency is sought by the holder of the indebtedness has the right to request the court in which the action is pending to determine the fair market value of the real property as of the date of the foreclosure sale."

This statute creates an important opportunity for borrowers and guarantors. Instead of accepting the foreclosure sale price, the court may determine the property's fair market value as of the foreclosure date.

Why Does This Matter?

Foreclosure sales frequently occur under distressed conditions. Properties may sell for less than what an informed buyer would pay in a normal transaction.

Recognizing this reality, Texas law allows the defendant to argue that the property's actual fair market value exceeded the foreclosure sale price.

If the court agrees, the lender's deficiency claim can be reduced.

How the Credit Is Calculated

Texas Property Code § 51.003(c) states:

"If the court determines that the fair market value is greater than the sale price of the real property at the foreclosure sale, the persons against whom recovery is sought are entitled to an offset against the deficiency in the amount by which the fair market value exceeds the sale price."

This means the borrower receives credit for the difference between:

- The foreclosure sale price; and

- The court-determined fair market value.

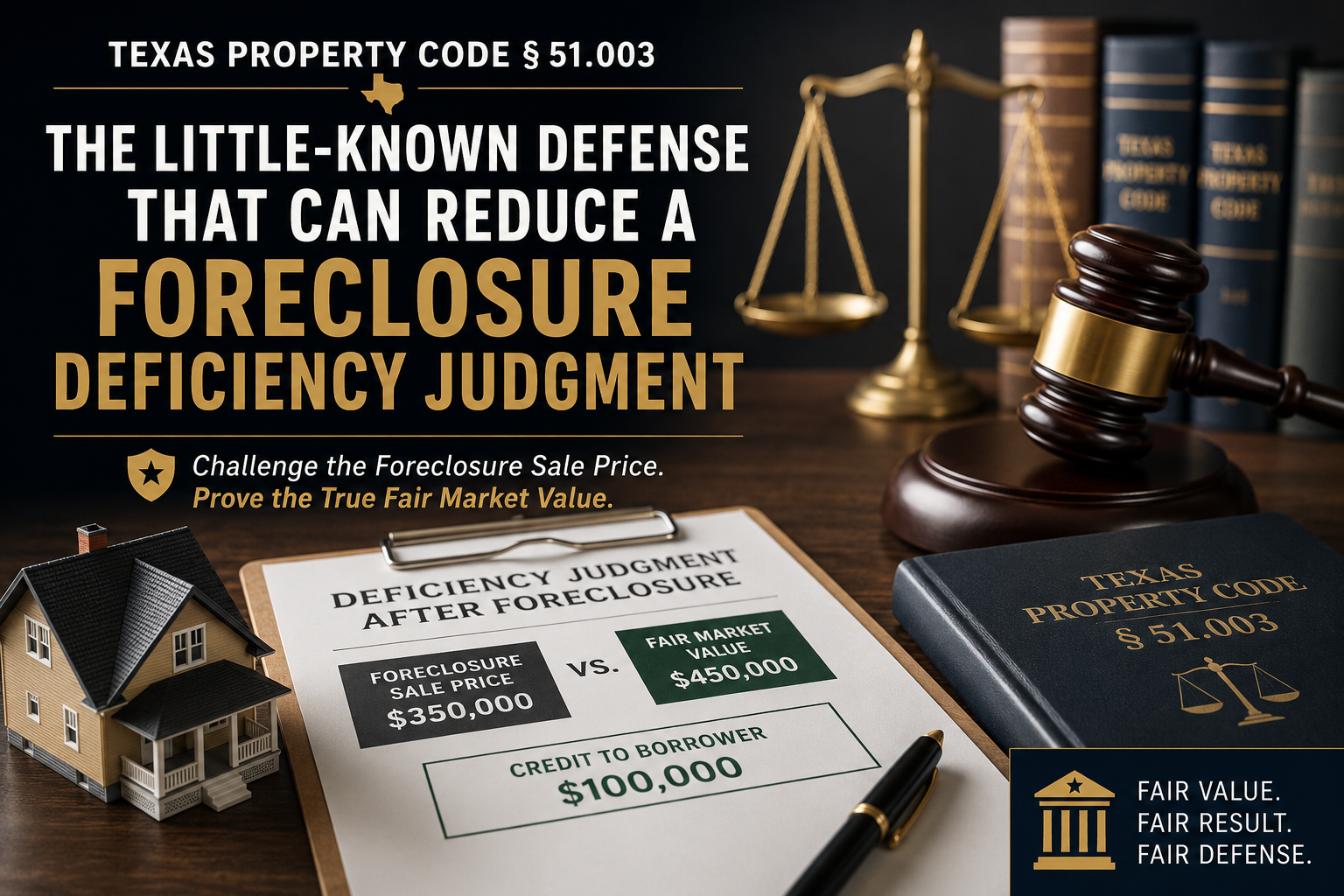

Example

Assume:

- Debt balance: $500,000

- Foreclosure sale price: $350,000

- Court-determined fair market value: $450,000

Without Section 51.003, the deficiency would be:

$500,000 − $350,000 = $150,000

With Section 51.003:

$500,000 − $450,000 = $50,000

The statutory valuation process reduces the potential deficiency by $100,000.

The Deadline Is Critical

Many borrowers lose this protection because they wait too long.

Texas Property Code § 51.003(b) provides:

"Any action brought to recover a deficiency must be brought within two years of the foreclosure sale."

While the statute establishes the lender's deadline for filing suit, defendants should raise the fair-market-value issue promptly once litigation begins. Waiting until late in the case can create procedural problems and increase litigation costs.

What Evidence Can Be Used?

Texas Property Code § 51.003(d) permits courts to consider a variety of valuation evidence, including:

- Expert appraisal testimony;

- Comparable sales;

- Property tax records;

- Income generated by the property;

- Condition of the property;

- Any other competent evidence of value.

Because valuation disputes often become a battle of competing experts, retaining a qualified appraiser can be critical.

Does the Statute Protect Guarantors?

Frequently, yes.

Texas courts have recognized that guarantors may invoke Section 51.003 in many circumstances when a lender seeks to recover a deficiency following foreclosure. This often becomes a major issue in commercial real estate litigation involving partnerships, LLCs, and investment properties.

Common Misconceptions

"The foreclosure sale price is automatically the property's value."

False. Section 51.003 specifically allows a court to determine fair market value independently of the foreclosure bid.

"Only homeowners can use this statute."

False. The statute often arises in commercial real estate disputes involving office buildings, retail centers, warehouses, and investment properties.

"The lender always wins."

Not necessarily. A significant difference between fair market value and the foreclosure sale price can dramatically reduce the claimed deficiency.

Practical Advice

If you are facing a deficiency lawsuit after foreclosure, do not assume the lender's numbers are correct. Texas Property Code § 51.003 gives defendants a meaningful opportunity to challenge the amount claimed and seek a fair valuation of the property.

Likewise, lenders should carefully evaluate the property's market value before filing a deficiency action. An inflated deficiency claim may be significantly reduced once fair-market-value evidence is presented.

Conclusion

Texas Property Code § 51.003 represents one of the most important—but often overlooked—protections available after foreclosure. By allowing courts to determine the property's actual fair market value rather than relying solely on the foreclosure sale price, the statute helps prevent borrowers and guarantors from being unfairly burdened by artificially low foreclosure bids.

Whether you are a lender seeking recovery or a borrower facing a deficiency claim, understanding Section 51.003 can dramatically affect the outcome of the case.

At David C. Barsalou, Attorney at Law, PLLC, we help clients navigate business, family, tax, estate planning, and real estate matters ranging from document drafting to litigation with clarity and confidence. If you’d like guidance on your situation, schedule a consultation today. Call us at (713) 397-4678, email barsalou.law@gmail.com, or reach us through our Contact Page. We’re here to help you take the next step.